During the course of buying the farm an interesting question came up about “buying points”. This was our first mortgage so I was pretty curious about everything going on with the banks and inspectors and such. Our lender casually mentioned the option of buying points and then quickly dismissed it as something that no one ever does. In fact, she had only seen it done once. When she said that I got even more interested.

I know not all beginning (or existing) farmers will be able to buy land, but for those who do I thought this topic would be helpful. There's not much good info about the trade-offs between buying points and putting down a larger down payment online, so this is just my own analysis, I'm very welcome to other opinions.

What’s “buying points”?

Buying points is basically paying a specified amount of cash upfront for a lower interest rate on the mortgage. A certain amount of dollars equate to a specific reduction in the interest rate. In our case the lender said we could “buy-down” up to two “points”. Each “point” was 0.25% off of our interest rate. If our interest rate was hypothetically quoted at 5.0% and we chose to buy two points our actual interest rate would be 4.5%.

Points May Make More Sense Than Higher Down Payment

The median US home price has hovered around $300,000 for the past few years, so let’s take a hypothetical example at that price. Let’s say you want to put down 20% on a $300,000, 30 year fixed-rate mortgage at a 5% interest rate. Due to your excellent credit the bank tells you that you could put down as little as 15%. If you put down 15% you would save $15,000 in upfront costs, but putting down 20% would save you close to $30,000 over the life of the loan. Sounds pretty good if you have the cash and you're not too optimistic about being able to invest that money in a higher yielding security. In the example of a mortgage you're effectively earning your interest rate on the extra money you put down, or 5% per year in this instance.

The loan officer also tells you that you could buy points and that it would lower your interest rate by 0.25% for each point. At most you could buy 2 points and your interest rate would go from from 5% to 4.5%. He says that each point costs $2,500 (this amount will vary depending on the bank and current rates at the time). So for an incremental $5,000 (for two points) you could pay a 4.5% rate.

The loan officer also tells you that you could buy points and that it would lower your interest rate by 0.25% for each point. At most you could buy 2 points and your interest rate would go from from 5% to 4.5%. He says that each point costs $2,500 (this amount will vary depending on the bank and current rates at the time). So for an incremental $5,000 (for two points) you could pay a 4.5% rate.

Now you're faced with a decision. You can’t afford to put down 20% AND buy the additional points, so you need to figure out which option is better.

You already know that for an additional 5% down ($15,000) you would save $30,000 over the next 30 years. The question is what would buying points save you over the life of the loan?

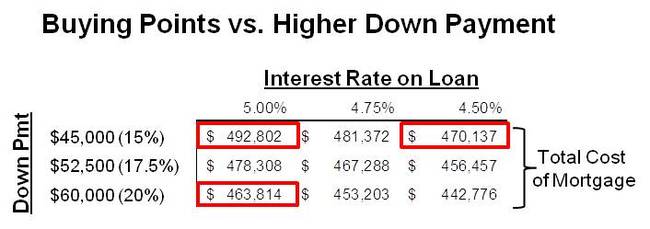

Here’s a table showing the various outcomes based on different down payments and different interest rates. The numbers in the middle of the table are the total cost of the mortgage over the life of the loan. Included in the 4.75% and 4.5% columns are the incremental $2,500 and $5,000 cash costs for buying the associated points.

As you can see, the cost of a $300,000 mortgage with 20% down and a 5% interest rate will be $463,814 over 30 years. The same mortgage with 15% down would cost $492,802 in total. The additional $15,000 you put down at the beginning would save $29,000 over 30 years.

If you buy two points for $5,000 and put 15% down you’ll end up paying $470,137 over the life of the loan. Compared to not buying points you are saving close to $23,000.

So in these two situations you can either put $15,000 down and save $29,000 or put $5,000 down and save $23,000. Which would you rather do? Putting more down on the home will earn you a return of 5% per year (your interest rate). Meanwhile, buying points and staying in the home for 30 years will earn you closer to a whopping 15% per year. Try to beat that in the stock market (actually don't, just buy the points).

Taken one step further you could take the $10,000 difference and apply it to the principal right away and save even MORE money over the life of the loan.

You already know that for an additional 5% down ($15,000) you would save $30,000 over the next 30 years. The question is what would buying points save you over the life of the loan?

Here’s a table showing the various outcomes based on different down payments and different interest rates. The numbers in the middle of the table are the total cost of the mortgage over the life of the loan. Included in the 4.75% and 4.5% columns are the incremental $2,500 and $5,000 cash costs for buying the associated points.

As you can see, the cost of a $300,000 mortgage with 20% down and a 5% interest rate will be $463,814 over 30 years. The same mortgage with 15% down would cost $492,802 in total. The additional $15,000 you put down at the beginning would save $29,000 over 30 years.

If you buy two points for $5,000 and put 15% down you’ll end up paying $470,137 over the life of the loan. Compared to not buying points you are saving close to $23,000.

So in these two situations you can either put $15,000 down and save $29,000 or put $5,000 down and save $23,000. Which would you rather do? Putting more down on the home will earn you a return of 5% per year (your interest rate). Meanwhile, buying points and staying in the home for 30 years will earn you closer to a whopping 15% per year. Try to beat that in the stock market (actually don't, just buy the points).

Taken one step further you could take the $10,000 difference and apply it to the principal right away and save even MORE money over the life of the loan.

Drawback of Buying Points

Sounds too good to be true you say? Yes, there is one primary drawback. Buying points to get a lower interest rate does not result in increased equity in your home and you will not get the value out of your points unless you stay in the home long enough to benefit from the lower monthly payment. You are giving the bank money to guarantee you a lower rate, but if you're not in the home for a long enough period of time you won't save enough on the lower rate to recoup your initial investment.

How do you think about that? Basically, you just need to figure out how many years of your lower monthly payment will equate to the cost of buying points. In my example buying points would save you about $80 per month, or about $950 per year. At an initial cost of $5,000 you will earn back the cost of your points in a little over 5 years.

This means that if you think you’ll be in your home for at least 5 years then you should buy the points. If you’re planning on flipping the home or there’s a high probability that you’ll move then don’t buy the points. Let’s take a case where you don’t think you’ll move before 5 years, but after 3 years you end up moving. It’s not the end of the world. You made back close to $3,000 ($950 x 3) and it cost you $5,000, so you lost $2,000. When compared to the opportunity to save close to $23,000 in the long term it’s not that big of a loss.

How do you think about that? Basically, you just need to figure out how many years of your lower monthly payment will equate to the cost of buying points. In my example buying points would save you about $80 per month, or about $950 per year. At an initial cost of $5,000 you will earn back the cost of your points in a little over 5 years.

This means that if you think you’ll be in your home for at least 5 years then you should buy the points. If you’re planning on flipping the home or there’s a high probability that you’ll move then don’t buy the points. Let’s take a case where you don’t think you’ll move before 5 years, but after 3 years you end up moving. It’s not the end of the world. You made back close to $3,000 ($950 x 3) and it cost you $5,000, so you lost $2,000. When compared to the opportunity to save close to $23,000 in the long term it’s not that big of a loss.

The other drawback for a lot of people is the cash cost. In some instances it might make sense to not buy-down points and take the 15% down payment and run with it. However, my example is comparing whether to put more money on a down payment or to buy points, I'm assuming your liquidity is not a concern.

Why Do Banks Offer Points?

I don't know this for sure, but my best guess is that banks offer points because they know that the average life of a mortgage in the United States is slightly over 6 years. Banks get the cash for the points upfront and can invest that money at the prevailing interest rate. They can price the points such that the payback duration is roughly equivalent to the average life of a mortgage in their lending area and over time they will make money on the float.

This is where you, as a dedicated farmer, can take advantage. Points exist because home-flippers, overzealous American borrowers and a generally finicky, gotta-have-a-new/bigger/whatever-house people exist. Those people drive down the average life of a mortgage. If you know that you'll be happy with your home and plan to stay on your land for a long time then you can save A LOT of money. Remember, these are your after-tax dollars, so gross up the savings for your tax rate if you want to see how much of your annual wages you'd be saving.

One final CYA disclaimer: I am not your financial advisor. This is not financial advice. Don't rely on this analysis to form your investment opinions. Before you make your own decision please perform your own analysis, or hire someone to do it for you.

For the nit-picking financial wizards out there I do realize that in none of these analyses have I taken into account the time-value of money, which should put a value on deploying capital upfront. Given the low interest rates, highly volatile markets and increasing risk of inflation I don’t have a lot of faith in assuming a fair rate of return on my cash.

For the nit-picking financial wizards out there I do realize that in none of these analyses have I taken into account the time-value of money, which should put a value on deploying capital upfront. Given the low interest rates, highly volatile markets and increasing risk of inflation I don’t have a lot of faith in assuming a fair rate of return on my cash.